The London Metal Exchange (LME) Index hit a two-year high in May when funds surged into base metals, chasing a narrative of manufacturing recovery, super-charged energy transition demand and constrained supply.

Doctor Copper, investors’ favourite barometer of industrial activity, soared to an all-time high, spurred by a ferocious squeeze on the CME contract.

Both gold and silver markets also climbed as the metals complex returned to the investor spotlight after years of neglect.

However, the base metals rally faltered over June as bullish expectations collided with the reality of high inventories and soft demand in China, the world’s biggest metals user. The LME Index is 10% off its late May highs.

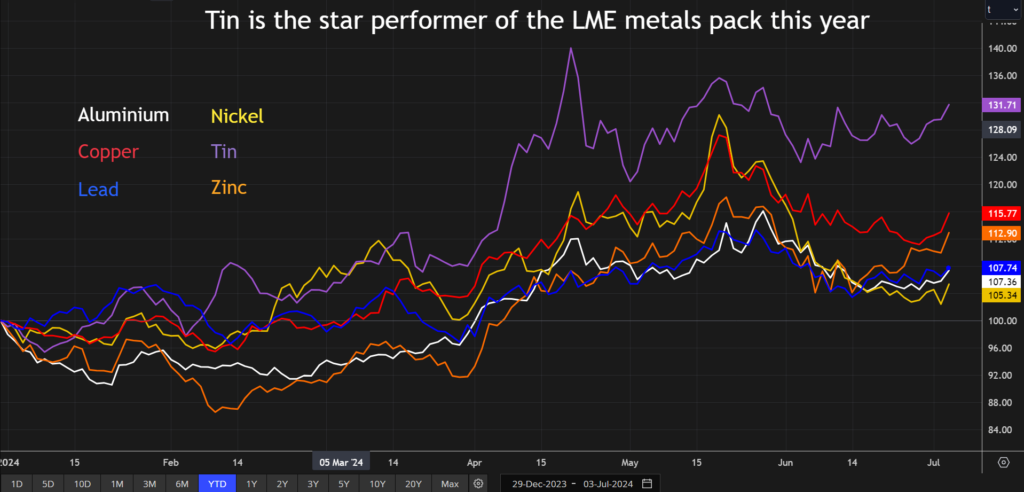

Only one LME base metal has held firm in the broader price retreat. LME tin , trading around $33,250 per ton, is up by 31% on the start of the year, out-performing the others by a wide margin.

While funds have focused on future supply constraints for metals such as copper, tin supply is disrupted in the here and now.

Funds and Optics

Tin has been lifted by the broader rotation of speculative money into the base metal sector.

Fund long positioning stretched to 3,781 contracts in April, the most bullish reading since the LME launched its Commitments of Traders Report in 2018.

While funds were busy reducing long positions in other metals last month, they held those in tin. Investor long positions were a sizeable 3,726 contracts at the close of last week.

Fund managers have no cause to sell. The price has been steady and LME stocks of the metal have fallen.

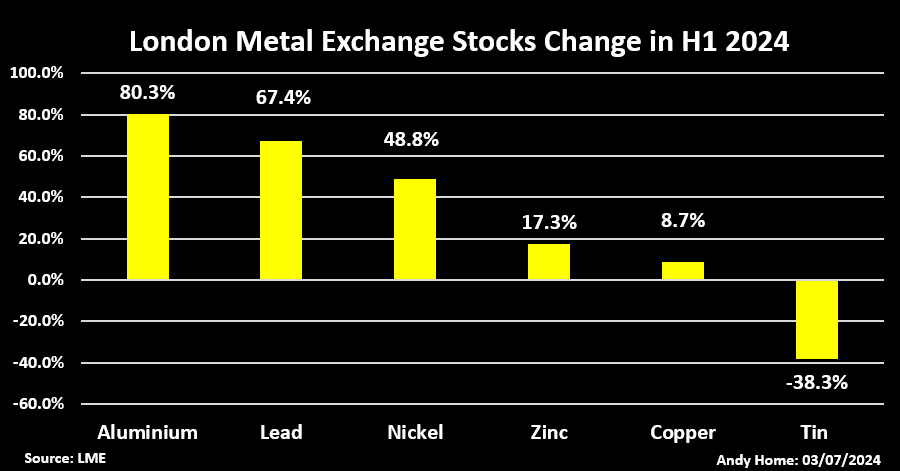

Overall LME inventory rose from 1.16 million to 1.79 million metric tons in the first half of the year. Much of that increase was down to a dump of aluminum into the system in May but exchange stocks risen across the board.

LME tin stocks, by contrast, fell by 38% to 4,750 tons over the first six months of 2024.

True, stocks registered with the ShFE are higher at 15,127 tons but they too have been sliding and are 15% off their May peak.

Exchange stocks are not always a reliable guide to fundamentals but bullish optics do no harm to a bullish market narrative.

Just ask Doctor Copper!

Copper bulls have been wrong-footed by a recent steady inflow of metal into LME warehouses and high Shanghai Futures Exchange (ShFE) inventory. Shanghai stocks have conspicuously failed to follow the seasonal pattern of rapid decline after the Lunar new year holidays.

The optics are doubly negative, implying weak demand and plentiful availability of metal, undercutting a narrative of constrained supply and market deficit.

Supply Constraints

A lack of long-term supply growth is core to the bull case for metals such as copper, zinc and increasingly aluminum.

Both copper and zinc show signs of tightness in the raw material segment of the supply chain, which helps to explain why they were second and third best performers in the first half of the year.

Smelter treatment charges have collapsed in both markets as mine supply struggles to keep up with demand.

However, a shortage of mined concentrates does not necessarily imply immediate tightness in the refined metal segment of the market, particularly if it is the result of increased smelter demand.

New smelter capacity in the copper market and reactivated capacity in the zinc market have played as important a role in collapsed treatment charges as faltering mine output.

Against such a backdrop, low treatment charges may translate into slower production growth rather than a fall in refined metal output.

Tin, by contrast, has this year experienced both raw material and refined metal tightness.

Shipments of refined tin from Indonesia, the world’s largest exporter, have been severely disrupted by a backlog in issuing new licences. Outbound volumes slumped to 10,292 tons in January-May from 23,887 tons in the year-earlier period.

Flows of raw material from the Wa State tin mines in Myanmar to Chinese smelters have slowed considerably since the authorities initiated a wide-ranging audit in August last year.

China’s imports from Myanmar have fallen by 27% year-on-year so far in 2024 with the slowdown particularly pronounced in April and May,

The combination of reduced concentrate flows from Myanmar and refined metal flows from Indonesia that has served to force buyers to draw on exchange stocks both on the LME and in China.

Hitting the Pause Button

The second quarter rally in base metals looks like something of a false start.

Investors have been left waiting for reality to catch up with their bullish expectations.

While some of the speculation has froth has been blown off in June, plenty of investors have stayed with the broader bull story. Copper remains the top metallic play, judging by the mood at last week’s LME Asia seminar.

The take-away for bulls is that their case is stronger when there are tangible signs of a shortfall of metal in the form of declining visible inventories.

Tin is the only market where stocks are falling in response to supply disruption, which is why it has so clearly out-performed the rest of the LME pack in the first part of 2024.

Source: Mining.com

{kind=link}